Business line of credit sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail and brimming with originality from the outset. A business line of credit is a flexible financing option that allows entrepreneurs to borrow funds as needed, rather than taking a lump sum loan. This method of financing provides businesses with the liquidity to navigate cash flow fluctuations, invest in growth opportunities, and manage unexpected expenses.

Understanding the distinct advantages of a business line of credit compared to traditional loans can empower business owners to make informed financial decisions. By exploring various types of credit lines, eligibility requirements, application processes, and effective management strategies, this overview highlights how a business line of credit can play a pivotal role in sustaining and growing a business amidst the evolving financial landscape.

Understanding what a business line of credit entails

A business line of credit is a flexible financing option that allows businesses to access funds as needed, up to a specified limit. This financial tool is particularly significant in the business landscape as it provides companies with the liquidity necessary to manage cash flow, invest in opportunities, and navigate unexpected expenses smoothly. Unlike traditional loans that offer a lump sum upfront, a line of credit functions more like a credit card, where businesses can withdraw funds, repay them, and borrow again as required.

Differences between a business line of credit and traditional loans

Understanding the distinctions between a business line of credit and traditional loans is crucial for businesses when deciding the best financing option for their needs. A business line of credit offers flexibility in borrowing, which differs significantly from the structure of traditional loans. Key differences include:

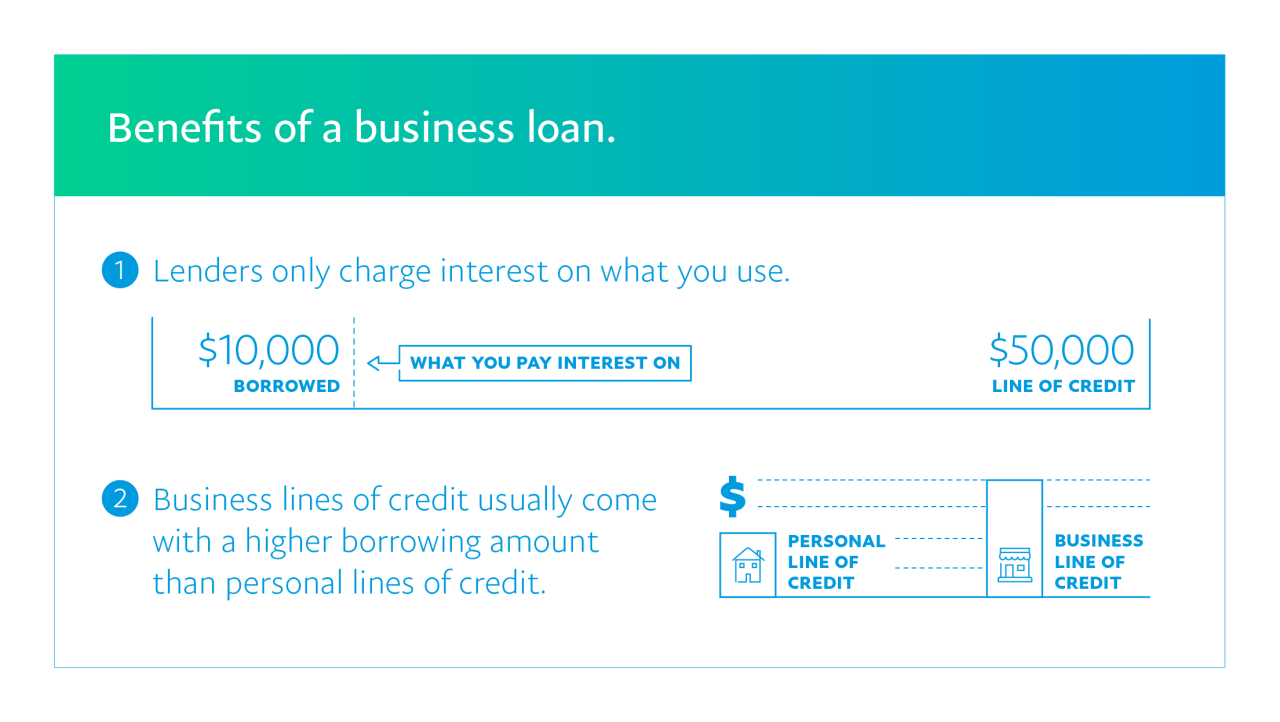

- Access to Funds: A business line of credit allows businesses to draw funds as needed, whereas traditional loans provide a one-time disbursement.

- Interest Payments: Interest is only paid on the amount drawn from a line of credit, while traditional loans require interest payments on the entire loan amount from the start.

- Repayment Flexibility: Lines of credit typically have more flexible repayment terms compared to the fixed repayment schedules of traditional loans.

Examples of scenarios where a business line of credit is beneficial

Business lines of credit are advantageous in various situations, allowing companies to respond quickly to financial needs without the constraints of traditional lending. One prevalent scenario is when businesses face seasonal fluctuations in cash flow. For example, a retail store might utilize a line of credit to stock up on inventory before the holiday season and repay the borrowed amount once sales surge.Another scenario involves unexpected expenses, such as a sudden equipment breakdown for a manufacturing company.

Accessing a business line of credit enables the company to cover the repair costs without disrupting operations.Additionally, businesses aiming to seize growth opportunities, such as expanding into new markets or launching new products, can use lines of credit to fund marketing campaigns or initial investments, ensuring they remain competitive.

“A business line of credit provides the flexibility to manage cash flow effectively while allowing for growth and unexpected expenses.”

The various types of business lines of credit available to entrepreneurs

Business lines of credit provide flexible financial solutions for entrepreneurs, allowing them to access funds as needed. It’s essential to understand the different types available, as each has unique features, benefits, and implications for your business. This knowledge can help you make informed decisions when seeking financing to support your venture.

Secured and Unsecured Business Lines of Credit

Understanding the distinction between secured and unsecured lines of credit is crucial for entrepreneurs. Secured business lines of credit require collateral, such as property or inventory, to back the borrowed amount. This collateral reduces the lender’s risk, often resulting in lower interest rates and higher credit limits. However, the downside is that failure to repay could lead to the loss of the asset used as collateral.Conversely, unsecured business lines of credit do not require collateral.

This option is typically faster to obtain and involves less risk to personal assets. Nevertheless, lenders often compensate for the higher risk through higher interest rates and more stringent credit requirements. Choosing between secured and unsecured credit depends on your business’s financial situation and risk tolerance.

Short-Term versus Long-Term Lines of Credit

When considering a business line of credit, distinguishing between short-term and long-term options is essential. Short-term lines of credit generally have repayment terms of up to 12 months and are ideal for covering immediate expenses, such as inventory purchases or unexpected operational costs. These lines are suitable for businesses with fluctuating cash flows that need quick access to funds.On the other hand, long-term lines of credit typically have repayment periods extending beyond a year, making them appropriate for larger investments like expansion or equipment purchases.

They offer more extended access to funds, allowing businesses to manage larger expenses more effectively. Selecting the right term aligns with your business needs and financial strategy.

Types of Lenders Offering Business Lines of Credit

A variety of lenders provide business lines of credit, each with distinct advantages and considerations. Traditional banks often offer competitive interest rates and favorable terms, but the application process can be lengthy and require substantial documentation.Alternative lenders, including online financial institutions and credit unions, typically offer faster approvals and more flexible criteria. These lenders are particularly beneficial for startups or businesses with less established credit histories.

However, they may charge higher interest rates in exchange for convenience and speed.Examining potential lenders carefully can help you choose one that aligns with your business needs. Consider not only the interest rates but also the lender’s reputation, customer service, and the overall terms of the credit line offered.

Key eligibility requirements for obtaining a business line of credit

When businesses seek a line of credit, lenders require certain eligibility criteria to be met. Understanding these requirements is crucial for business owners looking to secure funding. These criteria typically revolve around the financial health of the business and the overall creditworthiness of the owner or the company itself.Lenders assess various factors when evaluating applications for a business line of credit.

The common criteria they consider include the business’s credit score, financial history, annual revenue, time in business, and debt-to-income ratio. Each of these factors plays a significant role in the decision-making process, as they collectively help lenders gauge the risk involved in extending credit.

Importance of credit scores and financial history

Credit scores and financial history are fundamental components in the approval process for a business line of credit. A strong credit score indicates to lenders that the business has a history of managing its debts responsibly. This score is typically calculated based on several factors, including payment history, amounts owed, length of credit history, types of credit used, and new credit.For small businesses, a credit score above 700 is often considered excellent and can significantly improve the chances of approval.

On the other hand, a score below 600 may hinder the ability to secure credit. Lenders also review the financial history of the business, including past loans, repayment patterns, and any bankruptcies or defaults.To enhance their chances of securing a line of credit, businesses can adopt several strategies. Regularly monitoring their credit report for inaccuracies and disputing any errors can lead to a higher credit score.

Additionally, maintaining a low debt-to-income ratio and ensuring timely payments on existing obligations demonstrates financial responsibility.Establishing a solid business plan that Artikels revenue projections can also be beneficial. Furthermore, maintaining accurate financial statements and tax returns helps convey transparency to lenders. By implementing these strategies, businesses not only improve their credit profiles but also present a compelling case to lenders for why they should be granted a line of credit.

The application process for a business line of credit

Applying for a business line of credit is a structured process that requires thorough preparation and understanding of the requirements involved. Successfully navigating this process can provide your business with the necessary financial flexibility to manage expenses and seize growth opportunities. This guide Artikels the steps involved, essential documentation, and common pitfalls to avoid during the application process.

Steps in the application process

The application process for a business line of credit involves several key steps. Each step is crucial in ensuring that your application is complete and presents your business in the best possible light.

1. Gather Necessary Documents

Collect all required financial documents to demonstrate your business’s creditworthiness.

2. Check Your Credit Score

Ensure your business and personal credit scores are in good standing, as they significantly impact the approval decision.

3. Choose a Lender

Research various lenders to find one that suits your business needs in terms of interest rates, terms, and fees.

4. Complete the Application

Fill out the application form accurately, providing all requested details.

5. Submit the Application

Send your application along with the gathered documents to the chosen lender.

6. Await the Decision

The lender will review your application and documents before making a decision. Be prepared for follow-up questions or requests for additional information.

7. Review the Offer

If approved, review the credit offer to ensure it meets your expectations and needs before accepting it.

Checklist of necessary documentation

Having a checklist of required documents is vital for a smooth application process. Below is a list of commonly required documentation:

- Business plan outlining the purpose of the line of credit and financial projections

- Personal and business credit reports

- Tax returns for the last two years (personal and business)

- Financial statements, including profit and loss statements and balance sheets

- Bank statements for the last few months

- Ownership and operating agreements for the business

- Legal documents such as licenses, registrations, and permits

- Identification documents (e.g., driver’s license or passport) of the business owner(s)

Gathering these documents beforehand can significantly expedite the review process and help avoid delays.

Common pitfalls to avoid during the application process

Understanding potential mistakes can help in avoiding pitfalls that may hinder your application. Here are some common issues to be aware of:

- Incomplete or inaccurate application forms, which can lead to delays or rejections

- Not providing sufficient financial documentation, making it difficult for the lender to assess your creditworthiness

- Ignoring the importance of a good credit score; lenders often use this as a primary factor in their decision

- Failing to shop around for the best lender, which may result in higher interest rates or unfavorable terms

- Neglecting to understand the terms of the credit line offered, leading to unexpected fees or costs

By being mindful of these common pitfalls, you can improve your chances of a successful application and secure the funding your business needs to thrive.

How to effectively manage a business line of credit

Managing a business line of credit is essential for maintaining financial stability and fostering growth. Utilizing this flexible funding option responsibly can help avoid debt accumulation and keep your business on the right track. By implementing effective strategies, you can ensure that your credit line serves as a valuable tool rather than a financial burden.Monitoring your usage and making timely repayments are crucial components of responsible credit management.

A business line of credit can easily become a slippery slope if not handled with care. By keeping a close eye on your credit utilization and ensuring regular payments, you can maintain a healthy financial posture.

Strategies for Responsible Utilization

To effectively manage your line of credit, it’s important to utilize it responsibly. Here are some strategies to consider:

- Use for Short-Term Needs: Reserve the credit line for immediate expenses or opportunities that can yield a quick return on investment, such as inventory purchases or urgent repairs.

- Avoid Unnecessary Withdrawals: Only access funds when absolutely necessary. This helps prevent the temptation to overspend and accumulate debt.

- Set a Budget: Create a budget that includes your expected withdrawals and repayments to ensure you stay within your financial limits.

Monitoring your usage is just as important as the initial utilization of the credit line. Keeping track of how much you borrow and the repayments made can have a significant impact on your overall financial health.

Importance of Monitoring Usage, Business line of credit

Regular monitoring of your line of credit usage can help you identify spending patterns and adjust your financial strategy accordingly. Consider these points:

- Track Borrowing Activity: Use financial software or spreadsheets to log every withdrawal and repayment, which helps in understanding your cash flow better.

- Review Statements Regularly: Regularly check your credit statements for any discrepancies or unexpected charges, ensuring that you remain in control of your finances.

- Adjust Usage Based on Performance: If certain expenditures do not yield expected returns, reassess and limit future withdrawals to prevent further losses.

Timely repayments are another critical aspect of managing your business line of credit. They can prevent interest from piling up and keep your credit score in good standing.

Tips for Timely Repayments

To ensure you’re making timely repayments and maintaining a good credit standing, consider the following tips:

- Set Up Payment Reminders: Use calendar reminders or payment alerts to ensure you never miss a due date.

- Establish a Fixed Repayment Schedule: Create a structured repayment plan that aligns with your cash flow, making it easier to manage monthly payments.

- Make Extra Payments When Possible: If you have surplus cash, consider making additional payments to decrease your overall debt faster.

Setting limits on withdrawals is a proactive way to maintain your financial health and avoid overextending your credit capabilities.

Setting Withdrawal Limits

Establishing clear limits on how much you withdraw from your line of credit can significantly aid in financial management. Here are some effective strategies for setting these limits:

- Determine a Maximum Withdrawal Amount: Based on your cash flow and budget, decide on a maximum amount you are comfortable borrowing at any given time.

- Create Withdrawal Categories: Allocate specific amounts for different business needs (e.g., payroll, inventory, marketing) to prevent overspending in one area.

- Review and Adjust Limits Periodically: Reassess your financial situation regularly to adjust your withdrawal limits based on changing needs and performance.

By employing these strategies, you can effectively manage your business line of credit, ensuring that it remains a beneficial resource without leading to unnecessary debt accumulation.

The impact of interest rates and fees on a business line of credit

Understanding the implications of interest rates and fees is essential for businesses considering a line of credit. These financial factors can significantly affect the overall cost of borrowing and influence a company’s cash flow management. It’s vital to delve into the determinants of interest rates and the common fees associated with lines of credit to make well-informed financial decisions.

Interest rates determination and influencing factors

Interest rates for business lines of credit are primarily influenced by several key factors, including market conditions, the lender’s cost of funds, and the borrower’s creditworthiness. Generally, lenders assess the risk they are taking when extending credit to a business, which includes evaluating the credit score, business history, and financial performance.In addition to these factors, economic indicators such as the Federal Reserve’s benchmark rates, inflation rates, and overall economic growth also play a crucial role in determining interest rates.

For instance, a rise in the Federal Funds Rate may lead to higher interest rates for lines of credit, as lenders adjust their rates to maintain profitability.

“A borrower’s creditworthiness significantly impacts the interest rates offered on a line of credit; better credit often means lower rates.”

Common fees associated with lines of credit

Business lines of credit often come with various fees that can add to the overall cost of borrowing. Understanding these fees is crucial for businesses to accurately assess their potential expenses. Below are some common fees associated with lines of credit:

- Origination Fees: A one-time fee charged by lenders for processing the line of credit application. This can range from 1% to 5% of the credit limit.

- Annual Fees: A recurring fee that may be charged simply for keeping the line of credit open, typically ranging from $50 to $500.

- Draw Fees: Some lenders impose fees each time a business draws from its credit line, which can be a fixed amount or a percentage of the amount drawn.

- Late Payment Fees: If payments are not made on time, businesses may incur late fees, which can vary by lender but often are a percentage of the missed payment.

Awareness of these fees is essential, as they can compound the interest costs over time. Businesses should carefully review the fee structures of different lenders to understand their potential impact on overall borrowing costs.

Comparison of rates and fees from various lenders

Exploring different lenders can reveal significant variations in rates and fees, underscoring the importance of shopping around. Here is a comparative overview of interest rates and fees from a selection of lenders:

| Lender | Interest Rate | Annual Fee | Origination Fee |

|---|---|---|---|

| Lender A | 6.5% – 8.5% | $100 | 2% |

| Lender B | 7.0% – 9.0% | $50 | 3% |

| Lender C | 5.5% – 7.5% | $0 | 1% |

This table illustrates that while Lender C offers lower interest rates and no annual fee, other lenders may have different fee structures that could make them more competitive depending on the specific borrowing needs of a business. Ultimately, comparing rates and fees across multiple lenders can lead to significant savings and better credit management for businesses seeking financial support.

The benefits and drawbacks of using a business line of credit

A business line of credit can be a valuable financial tool for entrepreneurs and small business owners, providing immediate access to funds when cash flow becomes unpredictable. It serves to smooth out the financial bumps encountered during slow seasons or unexpected expenses. However, like any financial product, it comes with its own set of advantages and potential pitfalls that should be carefully considered.The most significant advantage of a business line of credit is the flexibility it offers.

Unlike a traditional loan, which provides a lump sum that must be repaid, a line of credit allows businesses to draw funds as needed and only pay interest on the amount used. This can be particularly beneficial for managing operational costs or funding short-term projects without committing to long-term debt.

Advantages of Accessing a Line of Credit

Having a line of credit readily available can lead to a range of benefits, particularly during times of cash flow uncertainty. Here are some key advantages:

- Immediate Access to Funds: Businesses can quickly access funds for urgent needs, avoiding delays that might affect operations.

- Interest Only on Used Amount: Companies pay interest only on the drawn funds, which can lead to significant savings compared to a standard loan.

- Improved Cash Flow Management: A line of credit can help businesses manage cash flow peaks and valleys more effectively, ensuring funds are available when needed.

- Building Credit History: Regular use and repayment of a line of credit can enhance a business’s credit score, improving future borrowing potential.

While the benefits of a business line of credit can be compelling, it is essential to recognize the potential risks involved.

Risks and Disadvantages of a Business Line of Credit

Using a line of credit can also present certain drawbacks, particularly if not managed carefully. Understanding these risks is crucial for making informed financial decisions.

- Potential for Accumulating Debt: Easy access to credit can lead to overspending, resulting in a cycle of debt that can be hard to escape.

- Variable Interest Rates: Many lines of credit come with variable interest rates, which can increase over time, raising the cost of borrowing unexpectedly.

- Impact on Cash Flow: If a business relies too heavily on credit, it may face difficulties managing cash flow when payments become due.

- Fees and Charges: Some lines of credit come with maintenance fees or other charges that can add up, potentially offsetting the benefits of having a flexible financial resource.

Real-life testimonials help illustrate both sides of using a business line of credit. For example, a small retail store owner reported that accessing a line of credit helped them purchase inventory during a seasonal lull, ultimately leading to a record holiday sales season. Conversely, a tech startup found itself in a tough spot after repeatedly drawing from its line of credit without a solid repayment plan, resulting in higher debt levels and interest payments that stifled growth.In summary, while a business line of credit can provide essential support during unpredictable cash flow periods, it is vital for business owners to weigh the advantages and disadvantages carefully.

By understanding the potential risks and planning accordingly, businesses can make better financial choices that align with their long-term goals.

Alternatives to business lines of credit for financing needs

When businesses seek financing, they often consider a variety of options based on their specific needs and circumstances. While business lines of credit are a popular choice due to their flexibility and accessibility, there are several other financing alternatives that can also serve businesses effectively. Understanding these options, along with their advantages and disadvantages, is crucial for making informed financial decisions.One common alternative to business lines of credit is traditional loans, which can provide a lump sum of capital.

Businesses can also utilize credit cards for short-term financing needs or leverage invoice financing to access immediate cash based on outstanding invoices. Each of these options presents different benefits and challenges, which can impact their suitability for different business scenarios.

Traditional Loans

Traditional loans are typically offered by banks or credit unions and involve borrowing a specified amount of money that must be repaid over a designated period, usually with interest. These loans can be secured or unsecured, based on the business’s creditworthiness.

Pros

Larger amounts of funding are often available.

Predictable repayment schedules facilitate budgeting.

Can improve credit scores if repayments are made on time. –

Cons

The application process can be lengthy and complex.

Requires collateral or a strong credit history for approval.

Early repayment penalties may apply.

Business Credit Cards

Business credit cards offer a convenient way for companies to make purchases and manage cash flow. They often come with rewards programs which can be beneficial for frequent business expenses.

Pros

Immediate access to funds for day-to-day expenses.

Flexible repayment options, with the ability to pay off balances over time.

Rewards programs can lead to discounts or cash back on purchases. –

Cons

High-interest rates can lead to debt accumulation if not managed carefully.

Credit limits may be lower compared to traditional loans.

Can negatively impact personal credit scores if the business owner’s credit is tied to the card.

Invoice Financing

Invoice financing allows businesses to borrow money against their outstanding invoices. This method provides immediate cash flow while waiting for clients to pay their bills.

Pros

Quick access to cash without taking on debt.

No need for collateral since invoices serve as the security.

Helps maintain a steady cash flow, which is crucial for operations. –

Cons

Fees can be higher than traditional financing methods.

Reliant on the quality of invoices; if clients delay payments, it can create problems.

Could strain relationships with clients if they feel pressured for early payment.

In choosing the best financing method, businesses should assess their specific circumstances, including cash flow needs, creditworthiness, and the purpose of the funds. For instance, businesses experiencing rapid growth may benefit more from a line of credit or invoice financing, while those seeking stability might opt for a traditional loan. Understanding the implications of each option helps in aligning financial strategies with broader business goals.

Future trends in business lines of credit

As businesses navigate an ever-evolving financial landscape, the future of business lines of credit is being shaped significantly by advancements in technology and fintech. These trends are not just enhancing the borrowing experience but also redefining how small businesses access and manage credit. By understanding these shifts, companies can better position themselves to leverage financial opportunities that align with their growth objectives.Technology and fintech are revolutionizing business financing by streamlining processes and increasing efficiency.

Digital platforms and automated lending solutions enable quicker applications and approvals, often reducing the time from weeks to mere hours. Traditional banks are increasingly adopting these technologies, which results in a more competitive environment. Businesses now have access to a wider array of financing options, including peer-to-peer lending and online credit providers that use alternative data to assess creditworthiness.

Emerging trends in lending practices

The lending landscape is witnessing several emerging trends that are particularly impactful for small businesses. Alternative lending models are gaining traction, providing flexible options tailored to unique business needs. The rise of AI and machine learning in credit assessments allows lenders to evaluate risk more accurately, which can lead to better terms for borrowers. The following points highlight notable trends in lending practices:

- Dynamic credit limits: Lenders are beginning to offer credit lines that adjust based on a business’s cash flow and sales performance, allowing for more responsive financing.

- Blockchain technology: This innovation promises to enhance transparency and security in lending transactions, potentially reducing fraud and improving trust between lenders and borrowers.

- Personalized lending experiences: Fintech companies are leveraging big data to create customized loan offerings that meet individual business needs, making financing more accessible.

- Sustainable lending practices: There is a growing emphasis on funding businesses that promote sustainable practices, aligning financial support with environmental responsibility.

The implications of these trends are profound, particularly for small businesses that may have previously struggled to secure credit. With more flexible terms and innovative assessment methods, even those with limited credit histories can find opportunities for growth.

Accessibility and terms of future lines of credit

The future of business lines of credit promises greater accessibility and more favorable terms. As fintech continues to evolve, small businesses are likely to experience more streamlined application processes that require less paperwork and provide quicker access to funds. This change will be critical for businesses needing immediate financial solutions to capitalize on market opportunities or manage unexpected expenses.Several factors are anticipated to influence accessibility and terms:

- Improved credit scoring models: As alternative data sources are increasingly used for credit assessments, businesses with nontraditional credit profiles may find it easier to secure lines of credit.

- Increased competition: The influx of new lenders in the market is driving down interest rates and improving loan terms, making credit more affordable for small businesses.

- Regulatory changes: Evolving regulations may encourage more flexible lending practices, ultimately enhancing access to credit for underserved markets.

- Integration of financial tools: Many fintech solutions now offer integrated platforms that combine accounting, cash flow management, and credit offerings, providing a comprehensive view of a business’s financial health.

As these trends take root, small businesses can expect a landscape that not only promotes growth but also fosters a more inclusive financial environment.

Summary: Business Line Of Credit

In summary, a business line of credit represents a vital resource for entrepreneurs seeking to enhance their financial agility. While it offers distinct benefits such as easy access to funds, it is essential to be aware of the potential pitfalls, including accruing excessive debt. By understanding the nuances of managing a business line of credit and considering alternatives, business owners can strategically position themselves for success in their financial endeavors.

Answers to Common Questions

What is the typical interest rate for a business line of credit?

Interest rates for a business line of credit typically range from 7% to 25%, depending on creditworthiness and lender policies.

How can I improve my chances of approval?

Improving your credit score, maintaining a positive financial history, and ensuring you have robust business plans can increase your approval chances.

Can I use a business line of credit for personal expenses?

No, using a business line of credit for personal expenses is generally prohibited and can lead to complications or penalties.

How often can I withdraw from my business line of credit?

You can withdraw funds as needed, up to your credit limit, but it’s advisable to manage withdrawals carefully to avoid overextending.

Is a business line of credit available to startups?

Yes, some lenders offer lines of credit to startups, but they may require personal guarantees or collateral.